Starting 1st August 2025, all international money transfers into Tanzania will be required to be processed through the Tanzania Instant Payment System (TIPS), according to a directive issued by the Bank of Tanzania. This marks a significant shift in the way cross-border payments are handled in the country, aiming to increase efficiency, compliance, and innovation across the financial ecosystem.

The directive mandates that all banks, mobile money operators, and financial service providers receiving inbound remittances must route these transactions exclusively through TIPS, the national real-time payment system managed by the Bank of Tanzania.

What Is TIPS?

The Tanzania Instant Payment System (TIPS) is a central payment infrastructure that facilitates real-time money transfers between financial institutions in Tanzania. Initially launched for domestic payments, TIPS has grown to support interoperability between banks, mobile money operators, and other financial players. The new directive expands TIPS’ role to handle all inbound international remittances.

This upgrade follows a period of system enhancements and stakeholder consultations. The Bank of Tanzania has now introduced a dedicated use case within TIPS specifically for managing international money transfer (IMT) transactions.

Key Policy Details

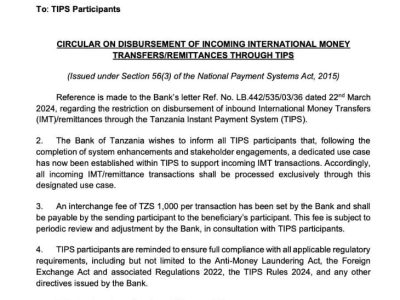

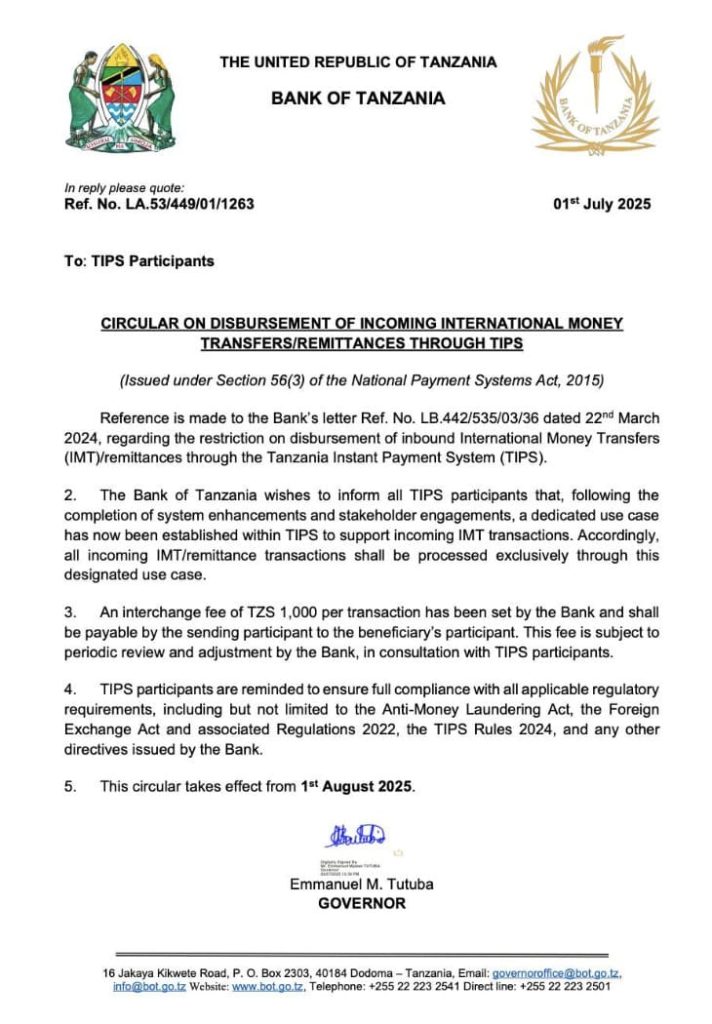

According to the official circular issued on 1st July 2025:

- All inbound international money transfers must be processed exclusively through TIPS, starting 1st August 2025.

- A fixed interchange fee of TZS 1,000 per transaction (approximately USD 0.38) will apply. This fee is payable by the sending institution to the receiving participant.

- All TIPS participants must ensure full compliance with Anti-Money Laundering (AML) laws, Foreign Exchange regulations, and other relevant rules issued by the Bank of Tanzania.

- The rule applies to all banks, mobile money operators, and other financial institutions integrated with TIPS.

Why This Change Matters

The directive represents a major evolution in Tanzania’s financial system. It is part of a broader trend across Africa to digitize financial services, improve regulatory control, and support innovation in cross-border payments.

Benefits of the New System

Faster Settlement:

Routing all transactions through TIPS means recipients will receive funds more quickly. Real-time settlement improves access and reduces delays, especially in rural or underserved areas.

Transparency and Predictability:

The flat fee of TZS 1,000 per transaction introduces consistency in pricing, eliminating the complexity and unpredictability that often accompanies cross-border remittances.

Stronger Regulatory Compliance:

TIPS enables better enforcement of financial regulations, including AML and foreign exchange rules. It provides the central bank with greater oversight and reduces the risk of fraud and illicit transfers.

Enablement of Fintech Innovation:

By creating a standardized infrastructure, this policy makes it easier for fintechs and new market entrants to integrate with the national system and offer compliant, efficient remittance solutions.

Better Data and Analytics:

Centralizing remittance flows into TIPS gives policymakers and regulators access to high-quality, real-time data, supporting better decision-making and planning.

Potential Challenges

While the directive offers clear benefits, it also introduces new challenges for financial institutions, remittance providers, and end users.

Integration Pressures:

Financial service providers must prioritize technical integration with TIPS to remain compliant. For those not yet fully integrated, the timeline may be tight, especially for smaller providers.

Impact on Small Transfers:

The fixed fee model, while transparent, may represent a significant cost for small-value transfers. For example, a fee of TZS 1,000 on a TZS 10,000 remittance translates to a 10% transaction cost.

Reduced Provider Flexibility:

Customers may have fewer choices in how they send and receive money. All providers must comply with the TIPS framework, which could limit differentiation and service customization.

Transition Risks:

Any major change in infrastructure carries risks of service disruption. Ensuring that all participants are ready and tested before the go-live date will be critical to avoid issues for customers.

A Step Toward Financial Inclusion and Digital Transformation

This shift positions Tanzania as a regional leader in digital payments and regulatory innovation. With an estimated USD 500 million flowing into the country each year through remittances, the new system is poised to make a significant impact on financial inclusion, especially among underserved populations.

By enabling real-time access to funds through both bank accounts and mobile wallets, the new TIPS requirement could improve household liquidity and strengthen the link between diaspora communities and the domestic economy.

At the same time, centralizing inbound remittances will help the Bank of Tanzania achieve more accurate monitoring of foreign currency flows and reduce reliance on informal channels.

How ClickPesa Supports This Transition

ClickPesa is fully integrated with the Tanzania Instant Payment System (TIPS) and ready to support this policy transition. For international remittance companies, financial institutions, and payment service providers looking to enter or expand in the Tanzanian market, ClickPesa provides a compliant, efficient, and user-friendly platform for cross-border transfers.

Our platform simplifies integration with TIPS, helps manage regulatory requirements, and ensures your customers can access real-time payment capabilities across Tanzania.

Whether you’re navigating the upcoming mandate or looking to improve your remittance infrastructure, ClickPesa can help.

Contact us today to learn how we can support your business ahead of the 1st August 2025 deadline.

How to Safely Make Payments to Safari Tour Operators in Tanzania

How to Safely Make Payments to Safari Tour Operators in Tanzania